Disclaimer: The article below discusses certain investment strategies, some of which I am currently using in my personal portfolio and some of which I am not. Do your own due diligence before making an investment decision. It’s your money; you’re the best person to judge what is best to do with it.

Balancing income growth with downside price risk is crucial to any portfolio, but especially if you are living off of your portfolio income. There’s an ongoing debate about whether a retiree’s portfolio should be managed with an income focus or a total return focus. An income focus seeks to generate as high of a yield as possible, through a combination of stock dividends and bond interest payments, with maybe some REITs and a few other instruments thrown in. A total return focus uses both income and underlying increase in prices to help fund withdrawals.

Allow me to be abundantly clear: a portfolio should always be managed with total return in mind. However, a pure focus on total return that many in the financial community ascribe to is a cop out. The income component of total return provides a valuable buffer against price volatility, because income is far less risky than price movements. Those living off of portfolio income must incorporate both return and risk into the investment strategy. Given the relatively low variability in income relative to price return, it makes sense to spend time seeking out income generating investments.

As discussed in a previous post, if you live strictly off your portfolio income and never touch the principal, you will never run out of money and market drawdowns will matter far less to you. Of course, that assumes that either your income is fairly stable and continues to grow by at least the rate of inflation, or you have a large enough capital base to allow reinvestment of some of the portfolio income. Both inflation and consistency in income matter –expenses for most people are relatively fixed on a month to month basis, but generally increase with broader prices over time. Large fluctuations in income without a large reserve balance can be a game-over moment – remember that companies and individuals don’t necessarily go bankrupt due to a cash flow issue, but rather a timing of cash flow issue.

Most middle income earners simply won’t be able to accumulate enough investment capital to live solely off of the income. At some point, they will have to sell some of the underlying investments. Selling any investment at any point increases the risk of not having enough money later in life. Remember that when you sell the underlying portfolio, it’s not only the return that matters, but the sequence of returns. Take a look at the below example. Both portfolios have the same return over the 25 year period, but because money is being withdrawn, a bad start really negatively impacts the final outcome.

Next to actually running out of money, inflation is the greatest risk that a retiree will face (although both risks are highly related). Retirees must plan ahead for decades without the potential for additional sources of income if the market does poorly. In the end, it’s a balancing act. A portfolio should provide a fairly stable income to help offset sequence of returns risk, while at the same time generating enough of a return to keep up with inflation. Stocks and stock dividends tend to keep up with, and over time exceed, the rate of inflation. Stocks also present the greatest downside and sequence of returns risk. Bonds, on the other hand, generate very stable income with very little downside risk, but generally don’t keep up with inflation.

Where to Get Income Growth and Where to Hide

There are plenty of ways to find portfolio income, but let’s start with the main two: stocks and investment grade bonds.

Stocks pay income through dividends, which are decided by the board of directors and can be cut at any time for any reason. For example General Electric always paid out and in fact, raised its dividend year after year, decade after decade…. until it didn’t. During the middle of 2009, they cut their dividend by 2/3rds, and just in the last few months, cut it in half. Worse, beyond the potential for a quick and sharp dividend cut like the 2/3rds cut by GE, stocks have both higher volatility and higher drawdown risk. At any time, although especially when living off of your portfolio, these risks must be balanced out.

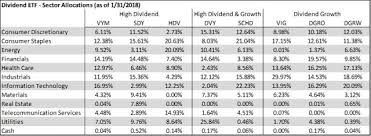

Dividend investors gravitate towards two main strategies: high dividends, or companies with dividend yields of 3.5-4% or higher, and dividend growth stocks, or companies that have lower yields (~1.5-2.5%) but are reinvesting a great deal in the business and expect to increase dividends in the future. Both have merit, although I tend to lean towards the dividend growth strategy, and there are several ETFs that allow you to buy a basket of these stocks without picking individual names. Diversity among companies and diversity among sectors are very important, and these ETFs offer a simple and cheap solution that provides both.

The balance comes from using a combination of strategies. High dividend stocks tend to grow less quickly and have less potential for growth, but often have lower price risk. Of course, since these companies are paying out greater amounts, they are reinvesting less in the business and may not be able to increase future dividends much. Lower yielding stocks tend to have greater volatility over time than higher payers, although that data is less clear. What is clear is that dividend paying stocks in general tend to move less than the overall market over time, though not always in specific environments. Assuming that high dividend payers will protect you during an economic decline can backfire.

On the other hand, bond income has been very stable but on a slow decline for decades. The great perk of bonds is the low downside risk, especially for US Treasury bonds and high quality investment grade corporate bonds. While dividends are not guaranteed and can be cut at any time, bond payments are contractual in nature and only bankruptcy can prevent their payment.

While dividend paying stocks have recently been seen as a good substitute for bonds given the low level of interest rates, they have much greater risk and should not be thought of as such. High quality bonds are often seen as a shelter in the storm during large drawdown periods, while dividend paying stocks decline substantially with the rest of the market. Further, dividends often decline during these tough markets, which is the worst possible time because the stock prices themselves have declined. Stock prices declined by a third or more from 2007 to 2009, at a time when dividends also declined substantially. The lower income from stocks would have required greater sells of the underlying portfolio at the worst possible time, accelerating your sequence of returns risk.

The biggest drawback to bond income is the lack of any kind of inflation protection. Inflation protected bonds, in the form of US TIPS and a few others, can offer stability in inflation adjusted income, but with a corresponding cost. They offer a very low yield. However, without that inflation kicker, you’ll lose out over time and suffer as a result. Most bonds have fixed coupons, meaning that you receive the same income each year until maturity, regardless of the inflationary environment. Worse, your principal returned at maturity will be the exact same amount as when issued, but with inflation, be worth far less.

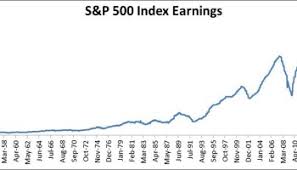

Dividends from stocks tend to grow through time, but as discussed above, can experience downturns. Bond income is very stable, but has been slowly declining for decades as the overall interest rate environment declines. The below chart shows the income generated each year from a $100 investment in both the S&P 500 and the Barclays Aggregate Bond Index, with no reinvestment done at any point.

As seen above, stock dividends have tended to increase over time substantially, but with several periods of big, sudden declines. Bond payments have been much more stable, but steadily declining as interest rates declined from their highs in the 1970s and early 1980s. Those will likely be more stable, if not somewhat increasing, in the future, given how low interest rates are now and the likelihood of modest increases in the future.

Offsetting that income growth, however, is the price risk associated with both. Almost all “market risk” is really stock risk. Below are the price returns over the same time frame, again using the same $100 invested in 1976.

Here you can see that stock prices have been on quite a run and increasing over time while bond prices, because of their contractual nature, really have no ability to increase substantially. Great, just put all your money in stocks, right? Not so fast, because this can happen:

And this can happen:

And let’s not forget the big one:

What’s an Investor to Do?

Today’s market is particularly challenging. Stocks are expensive, and bond yields are low but rising. Depending on how quickly bond yields rise, or if they even continue to rise, the drawdown risk for bonds is greater and the diversification benefit is less than in the past.

Diversification is more crucial than ever, both among and within asset classes. However, diversification only gets you so far. It helps in normal markets but less so in markets with a sharp decline. Let’s use the S&P 500 (US Stocks) as a baseline, and then compare the performance during the 2008-2009 Global Financial Crisis to other assets. For our purpose, both depth of the drawdown, as well as the length of time needed to recover, are important.

As you can see, very little was able to squeak through without being harmed. Importantly, take a look at the different outcomes for dividend stock indices. Depending on your strategy, you had a 16% wide performance difference with an almost two year gap in recovery time. Further, look at the performance of convertible bonds. Convertible bonds are often preached to be the optimal combination of income with downside protection. During a financial crisis, nothing could be further from the truth.

High quality bonds, like US Treasuries and investment grade corporate bonds, seem to have performed well – which is absolutely true, as these were a shelter from the storm. The problem today is the different interest rate environment and the question of whether we can count on the same performance. For example, the 10yr Treasury yield reached over 5% in middle of 2007, and was still near 4% before the crisis hit. Today, it’s 2.4%. Bonds need their yields to decline in order to increase in price and today, there’s less room for bonds to run.

But back to the question of what an investor is to do. Having a long time horizon helps, as most assets tend to recover given enough time. Not everyone has the luxury of time though. If you are near retirement age, and not in the early retirement camp, then remember that you’ve got at least one good, inflation adjusted hedge in place – Social Security. Beyond that, covering your basics with things like an inflation-adjusted SPIA or a TIPS ladder can make sense. At this point in your life, removing the downside risks of outliving your money can be worth the extra costs that these strategies entail.

For the rest of us, it depends on your current financial position and how long you have left in the work force. For example, I’m still in my late 30s, so can continue to work if needed. All else equal, I’m favoring stocks relative to bonds. Over periods of 15 years or more, valuation of the stock market matters less than shorter time frames. Remember that a portfolio has to last for decades, so future growth is important, and that growth won’t come from bonds. And while this will be discussed in a later post, withdrawing money from stocks based on performance increases makes sense. For example, you can remove a chunk from your stock allocation and place it in high quality bonds if stocks increase by more than a pre-determined number (say 20% or 30%) from where you bought. Conversely, since stocks tend to recover fairly quickly (although it can still take years), you must do everything possible to not sell stocks after they’ve declined sharply. Hence, holding bonds as a downside buffer helps weather the storm. Beyond just performance, where investments are held- in either a taxable or tax-deferred account- matters. Stocks and stock dividends are taxed much more favorably than bonds, so if you hold these investments in a taxable account, bonds face a headwind relative to stocks.

Finally, there are other strategies than can be used to mitigate drawdowns in a risky portfolio. Combining things like momentum or trend-following with a carry strategy make a very drawdown resistant portfolio without giving up return. Trailing stop loss orders can be used to mitigate downside risk, as stocks do tend to trend in the short run. Option and volatility strategies can also have their place, assuming that you understand them well enough to know when you’ll do well and when you’ll do poorly. All of these have merit if used correctly. Simplicity, however, has its merits, so favor stocks, but remember that high quality bonds can make surviving a downturn much easier.

Keep building my friends.

Что делать инвестору?